Account Types, ETFs, Position Sizing, & Building a Base

Lesson two

Introduction

Welcome to the second lesson. For most, this one will be pretty boring. Hopefully you know all of this if you’ve been trading for a while. But for others, this will teach you basic financial concepts that you should know for the rest of your life.

If you don’t know the concepts that I outline in this article, then you barely know how the market works. But that’s exactly why I’m writing these. So that you can get a solid understanding of markets before you start using them to change your life.

Even still, there are some portions of this lesson that I think are crucial for even experienced traders. Especially towards the end.

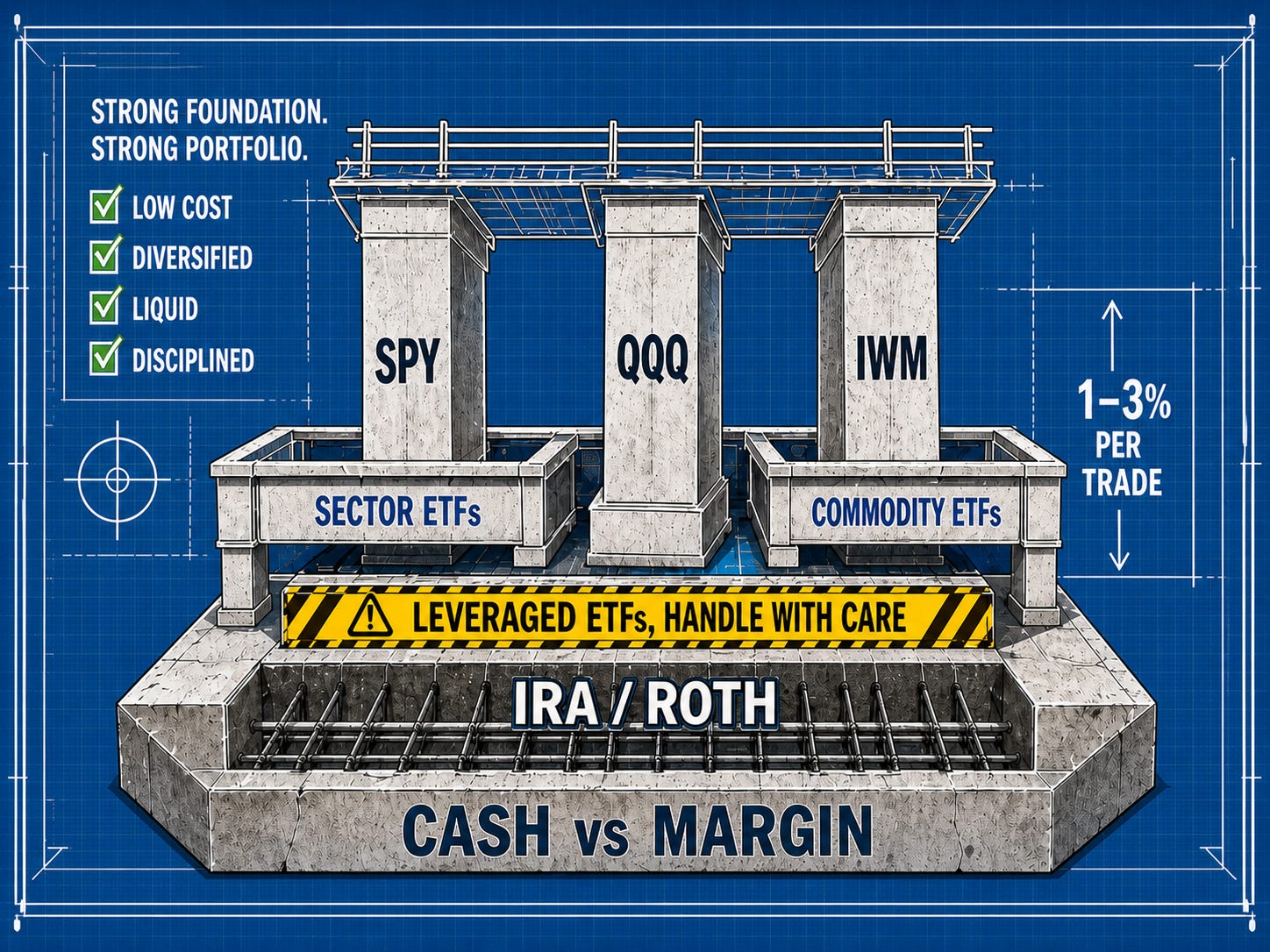

1. Cash Accounts, Margin Accounts, and the PDT Rule

When you open a brokerage account, you’re going to be asked to pick between a cash account and a margin account. This sounds boring. It is not. It controls what you’re allowed to do, how fast you can recycle capital, and whether you’re going to get a nasty surprise when you try to close a trade.

Cash Account

A cash account is exactly what it sounds like. You can only trade with money you actually have. When you sell something, the cash from that sale doesn’t fully “settle” for one business day on stocks (T+1) and one business day on options. Until it settles, you can’t use it again without triggering a violation. If you violate settlement rules a few times, the broker locks your account down for 90 days. Nobody wants that.

Margin Account

A margin account lets the broker lend you money against the value of your portfolio. You also get instant access to proceeds from sales, no waiting for settlement. For an active trader this is HUGE. You can sell a position at 10:00 AM and immediately use those proceeds to enter a new trade. In a cash account you’d be sitting on your hands until tomorrow.

The catch with margin: you can also borrow money. The broker will let you buy roughly 1.5x your account value in stock (not quite the correct math but close enough). This sounds fun. It is not always fun. Margin is how people go from a 30% drawdown to a margin call to a wiped account in a single bad week. I use a margin account because I want instant settlement and certain options strategies, not because I want to lever up with the margin itself. Big difference.

Pattern Day Trader

Now the rule everyone trips on, the Pattern Day Trader rule, or PDT. If your account is under $25,000 AND you’re in a margin account AND you make 4 or more day trades (open and close the same position on the same day) in a 5-business-day window, your broker will flag you as a PDT. Your account gets restricted. You typically can’t day-trade again until you bring the balance above $25K.

If you’re under $25K, you have basically three options:

Trade in a cash account, where the PDT rule doesn’t apply, but you have to deal with settlement

Trade in a margin account but stay under 4 day trades per 5-day window, track this carefully

Hold positions overnight (which by definition isn’t a “day trade”), this is what I’d recommend most beginners do anyway

If you’re under $25K, you should mostly NOT be day trading. Day trading is the hardest game in the market and the people who win at it have years of screen time. Build the account up holding overnight swings and longer-dated options first. That’s actually the better path even if PDT didn’t exist.

One important update on the PDT rule itself: it’s on its way out. In April 2026, the SEC approved FINRA’s proposal to eliminate the $25,000 minimum equity requirement for pattern day traders.[1] The new framework takes effect June 4, 2026, and brokers have until October 2027 to fully phase it in.[2] So depending on which broker you use and when you’re reading this, that $25K threshold may already be gone and replaced with a new intraday margin framework that doesn’t punish small accounts for trading actively.[3] Even so, my advice in the previous paragraph stands. Day trading being legal for small accounts doesn’t make it a good idea for small accounts.

[1] SEC, Order Granting Accelerated Approval of FINRA Rule 4210 amendment (PDT provisions), File No. SR-FINRA-2025-017: https://www.sec.gov/files/rules/sro/finra/2026/34-105226.pdf

[2] FINRA Regulatory Notice 26-10 (June 4, 2026 effective date; 18-month phase-in through October 20, 2027): https://www.finra.org/rules-guidance/notices/26-10

[3] Charles Schwab, “SEC Approves Scrapping $25,000 Day Trader Minimum”: https://www.schwab.com/learn/story/sec-approves-scrapping-25000-day-trader-minimum

2. Taxable, IRA, and Roth

Everything we just talked about lives inside a “taxable” brokerage account, meaning every time you close a profitable trade, you owe taxes on the gain. Short-term gains (held under a year) get taxed at your normal income rate, which for most people is brutal. This is one of the reasons I push people to also have at least one tax-advantaged account running in parallel.

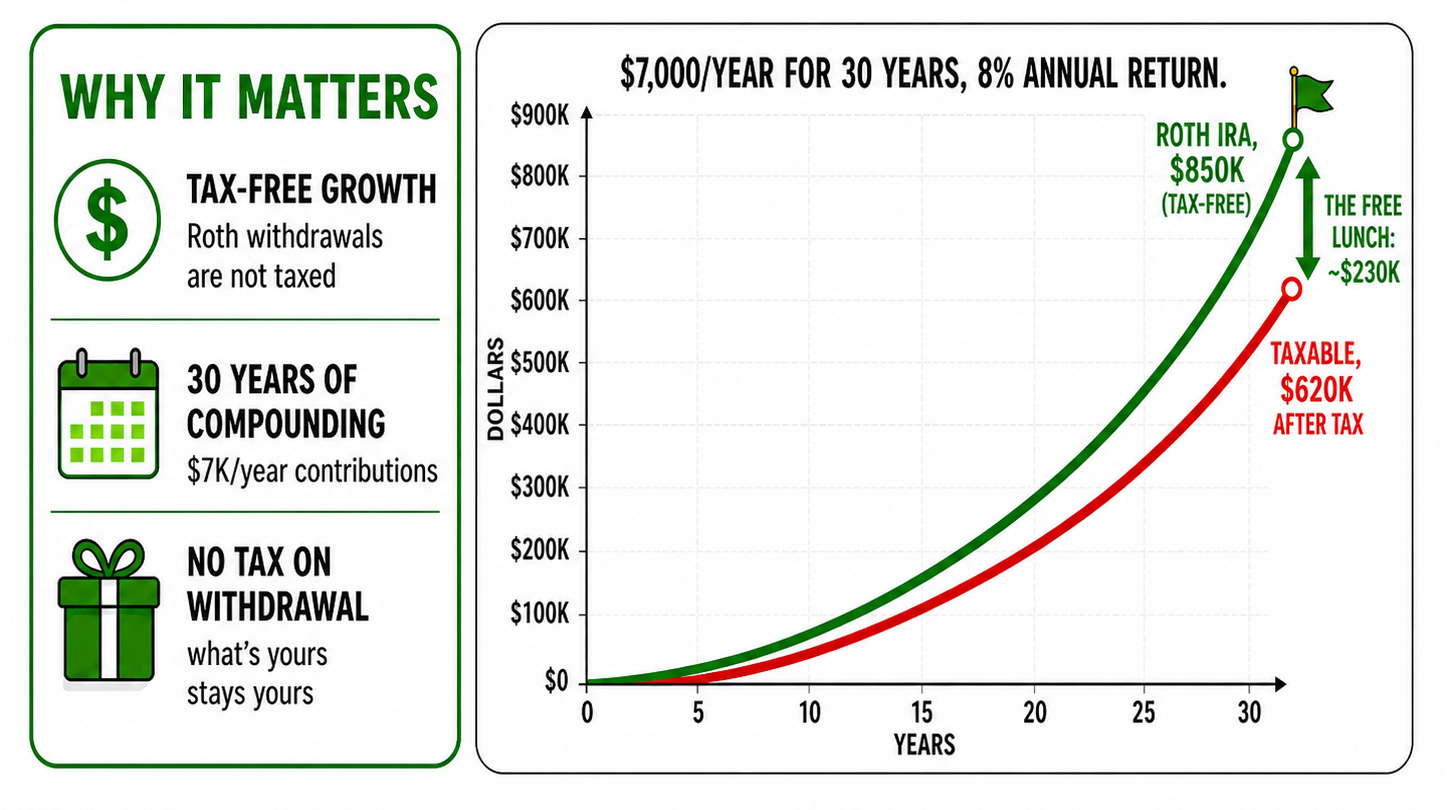

A Traditional IRA lets you contribute pre-tax money (up to a limit, currently $7,000/year if you’re under 50). That money grows untaxed. You only pay tax when you withdraw in retirement, ideally at a lower tax bracket than you’re in now. Good for high earners trying to reduce taxable income today.

A Roth IRA is the one I LOVE. You put in post-tax money (same $7K limit), but ALL the growth is tax-free forever, and your withdrawals in retirement are tax-free. If you’re young, or you think you’ll be making more later, or you just want one account where Uncle Sam can never come back at your gains, Roth is the move. There are income limits on direct Roth contributions, so if you make a lot, look up “backdoor Roth.”

And the good news is, you can ABSOLUTELY trade actively inside an IRA or Roth. Most brokers (Fidelity, Schwab, even Robinhood now) will let you buy and sell stocks, ETFs, and run basic options strategies inside a Roth. There’s no PDT rule the same way because IRAs are cash-only by structure (no margin), but options are still on the table at the right approval level. You can run cash-secured puts, covered calls, and even spreads inside a Roth at most brokers.

What you can’t do in an IRA: sell naked options, use real margin leverage, or short stock. Which is fine. Most of those things destroy retail traders anyway.

If I could only give you one piece of allocation advice for your first year: max out the Roth before you go nuts in the taxable. Tax-free compounding for 30+ years is one of the few mathematical free lunches in finance.

3. ETFs: The Base Layer of Everything

An ETF, exchange-traded fund, is a basket of stocks (or bonds, or commodities) packaged into one ticker that trades like a stock. You buy one share and you instantly own a slice of the whole basket. It’s the single most useful invention in modern retail investing.

There are three ETFs you’ll see me reference constantly:

SPY: tracks the S&P 500 (the 500 biggest U.S. companies). When people say “the market” is up or down, they almost always mean SPY or /ES futures.

QQQ: tracks the Nasdaq 100 (mostly big tech: AAPL, MSFT, NVDA, AMZN, META, GOOGL, etc.). Higher beta than SPY, meaning it moves bigger in both directions.

IWM: tracks the Russell 2000 (small-cap U.S. companies). Way more sensitive to interest rates and the domestic economy than SPY. When small caps rip while SPY does nothing, that usually tells you something about risk appetite.

If you only ever traded those three tickers and got really good at reading them, you could have a full career. They’re liquid, the spreads are a penny, the option chains are deep, and they ARE the market. There’s no “what’s this random small-cap going to do on earnings?”, you’re trading the whole economy.

Why ETFs matter as a base: any single stock can go to zero. Enron, Lehman, SVB, lots of cryptocurrencies. SPY can’t go to zero unless 500 of the biggest companies in America simultaneously die, at which point you have bigger problems than your portfolio. That structural diversification is what makes ETFs the foundation of basically every serious portfolio.

Sector & Commodity ETFs

Beyond the big three, there are sector ETFs that let you express a thesis on one part of the economy without having to pick the exact winner. The “SPDR Select Sector” group of ETFs is the most common: XLK for tech, XLF for financials, XLE for energy, XLV for healthcare, XLU for utilities, XLI for industrials, XLP for staples, XLY for consumer discretionary, XLB for materials, XLRE for real estate, XLC for communication services. You don’t need to know all of those, but I track them to see how different sectors of the economy are trading.

Sector ETFs are great when you have a macro view but don’t want single-stock risk. If you think rates are going to fall and banks are going to rip, you can buy XLF instead of betting on whether JPM specifically beats earnings. Cleaner thesis with smaller blowup risk.

Commodity ETFs are a separate animal. The ones I actually trade:

GLD: physical gold exposure. The classic “fear / debasement / dollar weakness” trade. Lower volatility than equities, completely different driver.

SLV: silver. Higher beta than gold, partly industrial demand, partly precious metal. Moves harder in both directions.

USO: oil. Tracks WTI crude futures (with some quirks we’ll get to). When geopolitics blow up or OPEC does something weird, USO is how retail plays it.

TLT: long-duration Treasuries. Technically bonds, not commodities, but I’m grouping it here because it’s another macro instrument. TLT goes UP when rates go DOWN. It’s a recession/risk-off hedge that also pays a yield.

Quick warning on commodity ETFs: most of them don’t hold the actual commodity, they hold futures contracts and roll them every month. In certain market structures (called contango), that rolling bleeds value over time. USO famously got destroyed in 2020 because of this. So commodity ETFs are great for tactical trades, but they are NOT long-term buy-and-hold instruments.

4. Leveraged ETFs: Not a Long-Term Hold

I will preface by saying that this section is VERY IMPORTANT.

Leveraged ETFs are not basis instruments. They use derivatives to give you 2x or 3x the daily move of an underlying index. So TQQQ is roughly 3x QQQ. SOXL is 3x semiconductors. SQQQ is -3x QQQ (it goes UP when tech goes DOWN). They’re extremely popular with retail because the daily moves are huge and exciting.

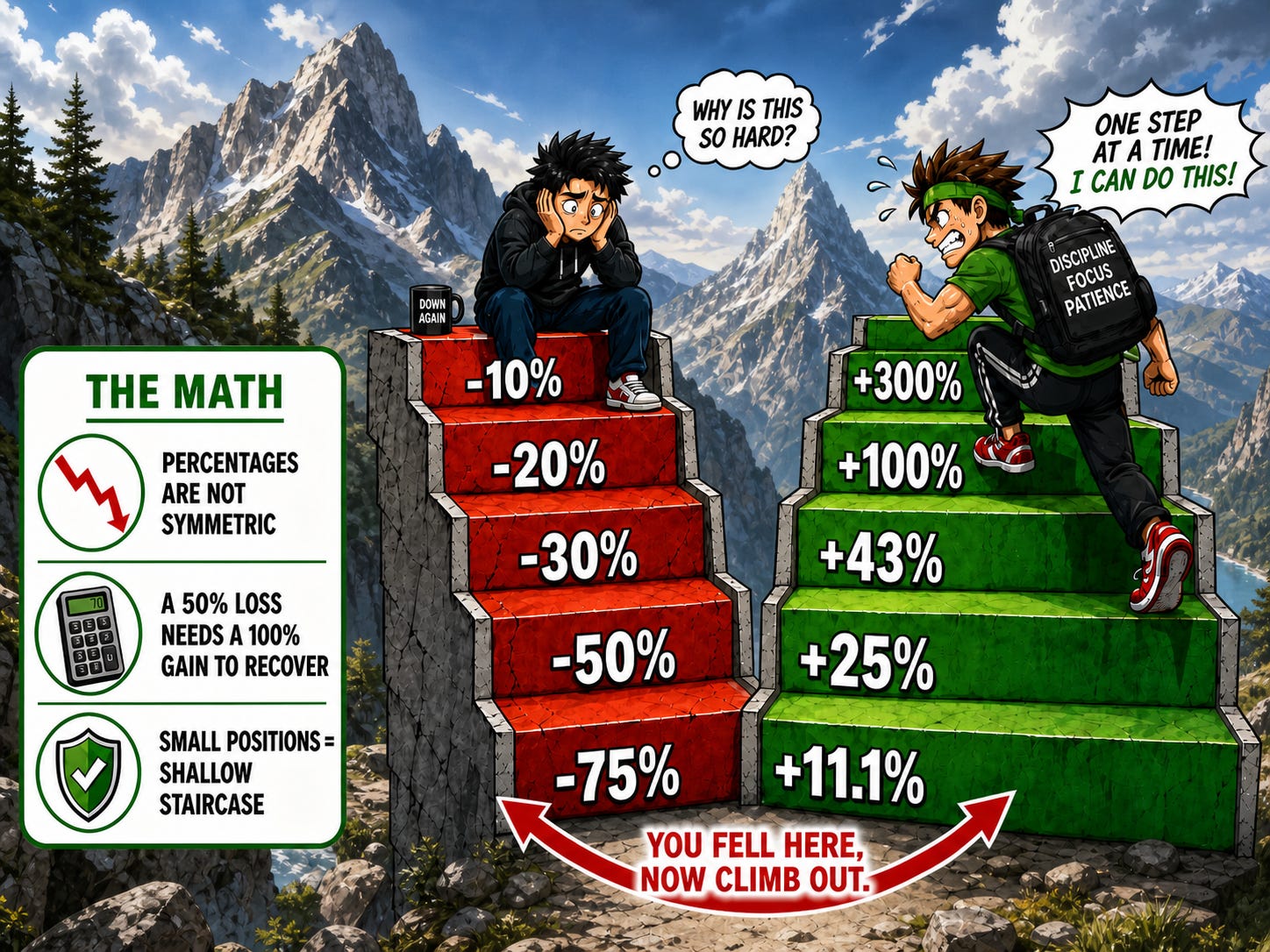

Here’s the thing nobody understands until it’s too late: those ETFs deliver 3x the DAILY return, not the long-term return. Because they reset every day, in a sideways or choppy market they bleed value through something called volatility decay. You can be RIGHT about direction over six months and still lose money holding a leveraged ETF if the path got chopped up.

This can be slightly difficult to understand, so don’t worry if you don’t get it at first.

What volatility decay actually is: percentage moves don’t cancel symmetrically. A 10% loss requires an 11.1% gain to get back to even, not a 10% gain. Leveraged ETFs amplify daily moves by 2x or 3x, which means they amplify that asymmetry too. Every up-down sequence chips a little off the top. The choppier the market, the more it bleeds. In a perfectly smooth uptrend, a 3x ETF can actually outperform 3x the underlying. But markets are almost never smooth, they mostly chop with occasional trends, which is why over time the math grinds against you. The longer you hold a leveraged ETF in a sideways market, the worse it gets.

Example. Imagine QQQ goes down 5% one day, then up 5% the next. Net move on QQQ: roughly -0.25% (because percentages don’t cancel). Same two days on TQQQ: down 15%, then up 15%. Net move on TQQQ: roughly -2.25%. Almost ten times worse. Now imagine that compounded over months of chop. This is why people who bought TQQQ at the top in 2021 and held it were down 80%+ at the lows even though QQQ itself wasn’t that bad.

My rules on leveraged ETFs:

Use them as TACTICAL tools, short-term directional bets, not long-term holds

Size them like options, not like stock, one bad week can shred you

Inverse leveraged ETFs (SQQQ, SPXS, etc.) are mostly hedge tools or short-term trades

DO NOT hold them for months and expect them to track the index

If you don’t fully understand volatility decay yet, just stay out of leveraged ETFs entirely until you do

5. Position Sizing 101

We’ll go deeper on sizing in a latter lesson completely focused on risk management, but I want to plant the seed here because everything else in this course is downstream of it.

Position sizing is just: how much money do you put in any one trade. That’s it. And it is, by a wide margin, the single biggest determinant of whether you make it as a trader. More than chart reading. More than picking good tickers. More than the Greeks. More than literally anything else.

I’m not going to hand you my exact sizing rules yet, those are personal and they’ve evolved over years of trades. What I’ll give you instead are some example rules of thumb that a beginner could start with and then modify as they get a feel for it:

On any single trade, you should be willing to lose 100% of what you put in without it changing your life or your psychology

For options trades specifically, that usually means no more than 1–3% of your total account per trade

For stock/ETF positions, you can go bigger because they don’t expire, 5–10% per name is reasonable for a high-conviction holding

To say it again because it matters: those are not the rules I personally use. My own sizing is different and it’s built around how I specifically trade. The point isn’t to copy someone else’s numbers, the point is that you NEED rules, you need to write them down, and you need to actually stick to them when you’re in the heat of a trade. A trader without sizing rules is just gambling with extra steps. Every trader I know who has lasted has a sizing framework they trust, and they don’t break it just because a setup looks great. Build yours, test it, refine it.

I know what you’re thinking. “1–3% per trade? I’ll never make any money.” Let’s do the math. If you’re sized correctly, a winning options trade returns 50–200% of premium. On a 2% position, that’s 1–4% on your total account, on a single trade. Stack a few of those a month and you’re crushing the index. Now imagine being wrong on a 20% position. You lose 20% of your account on ONE bad call. You now need to make 25% just to get back to even, on a smaller account, with damaged confidence. That’s the actual death spiral most retail traders enter.

Small size isn’t a lack of conviction. Small size is what lets conviction COMPOUND, because you’re still around to take the next trade. The traders making real money over years aren’t the ones swinging 30% positions. They’re the ones swinging 2% positions, hitting at 50%+, and running it back hundreds of times.

Burn this in: you don’t make money in this game by being right once. You make money by surviving long enough to be right a hundred times. Proper sizing is what gets you there.

Now you forget what you just read for two seconds while I explain a small caveat.

I’ll go over this more in the risk management lesson, but you need to understand something very important. Never forget this.

Diversification helps you stay rich, but concentration is how you get rich.

No one ever got rich by investing $100 into a diversified basket of stocks. And most traders didn’t get rich by limiting themselves to 1-3% of their account per trade. The most legendary investors have gotten to where they are through highly concentrated bets on high conviction investments.

If you have pocket aces, go all in.

But now I’ll circle back to the main piece of advice this section is supposed to emphasize: You don’t make money in this game by being right once. You make money by surviving long enough to be right a hundred times. Proper sizing is what gets you there.

What You Should Know After Lesson Two

The difference between cash and margin accounts, and what the PDT rule actually does to you

Why a Roth IRA is one of the best places on Earth to compound trading gains

What ETFs are, why SPY/QQQ/IWM are the core of the market, and what sector/commodity ETFs are good for

Why leveraged ETFs are tactical tools, NOT buy-and-holds, and what volatility decay does to your account

That position sizing, not stock picking, not chart reading, is the #1 driver of whether you survive long-term